Code

import numpy as np

import matplotlib.pyplot as plt

rng = np.random.default_rng(seed=42)In my previous post, I proposed a bet to a YouTube commenter who insisted the Monty Hall problem is a 50-50 coin flip. He declined to put money on it — so let’s let the computer settle things instead.

Below is a Monte Carlo simulation that plays the bet millions of times. The “stay” player always keeps Door 1; the “switch” player always switches to the remaining closed door after a goat is revealed. The payout terms: the switcher pays $1.08 when staying wins, and the stayer pays $1.00 when switching wins.

import numpy as np

import matplotlib.pyplot as plt

rng = np.random.default_rng(seed=42)ROUNDS = 10_000_000

SWITCH_BET = 1.08 # switcher pays this when staying wins

STAY_BET = 1.00 # stayer pays this when switching wins

DOORS = np.array([1, 2, 3])

STAY_DOOR = 1

# Randomly place the prize behind a door each round

winning_doors = rng.choice(DOORS, size=ROUNDS)

# Staying wins when the prize is behind Door 1

stay_wins = winning_doors == STAY_DOOR

# Switching wins whenever staying loses (the revealed door is never the prize)

switch_wins = ~stay_wins

stay_win_count = stay_wins.sum()

switch_win_count = switch_wins.sum()

# Net payouts

switch_net = switch_win_count * STAY_BET - stay_win_count * SWITCH_BET

stay_net = -switch_net

print(f"Rounds: {ROUNDS:>12,}")

print(f"Stay wins: {stay_win_count:>12,} ({stay_win_count / ROUNDS:.2%})")

print(f"Switch wins: {switch_win_count:>12,} ({switch_win_count / ROUNDS:.2%})")

print(f"Stayer nets: ${stay_net:>12,.2f}")

print(f"Switcher nets: ${switch_net:>12,.2f}")Rounds: 10,000,000

Stay wins: 3,333,698 (33.34%)

Switch wins: 6,666,302 (66.66%)

Stayer nets: $-3,065,908.16

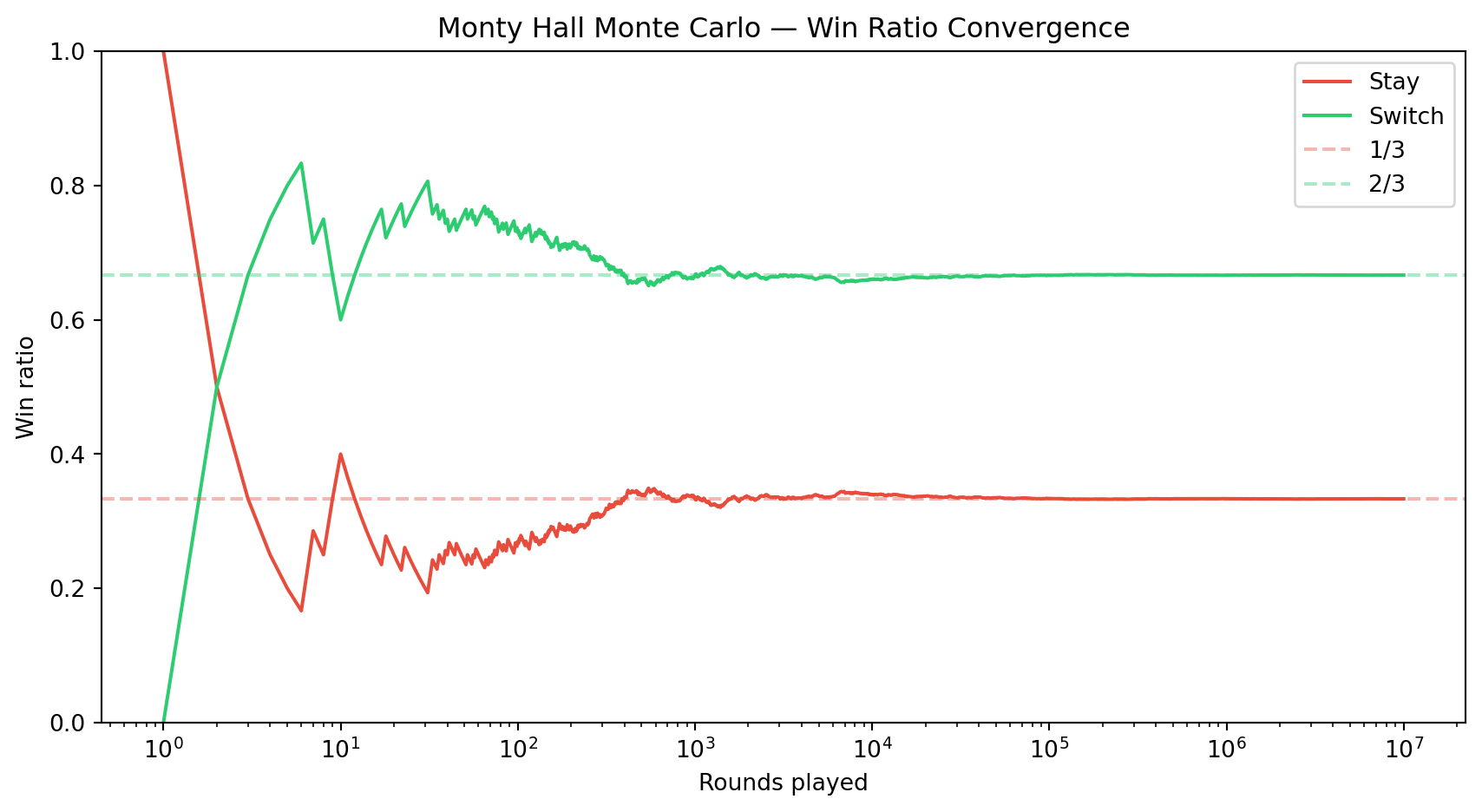

Switcher nets: $3,065,908.16Switching wins about 2/3 of the time — exactly as the math predicts. Even with the switcher paying an 8% premium on losses, the edge is overwhelming over millions of rounds.

As the number of rounds grows, the win ratios converge to their true probabilities: 1/3 for staying, 2/3 for switching.

cumulative_stay = np.cumsum(stay_wins)

cumulative_switch = np.cumsum(switch_wins)

rounds = np.arange(1, ROUNDS + 1)

# Sample points for plotting (log-spaced to keep the plot manageable)

idx = np.unique(np.geomspace(1, ROUNDS, num=2000).astype(int)) - 1

fig, ax = plt.subplots(figsize=(9, 5))

ax.semilogx(rounds[idx], cumulative_stay[idx] / rounds[idx], label="Stay", color="#e74c3c")

ax.semilogx(rounds[idx], cumulative_switch[idx] / rounds[idx], label="Switch", color="#2ecc71")

ax.axhline(1 / 3, color="#e74c3c", linestyle="--", alpha=0.4, label="1/3")

ax.axhline(2 / 3, color="#2ecc71", linestyle="--", alpha=0.4, label="2/3")

ax.set_xlabel("Rounds played")

ax.set_ylabel("Win ratio")

ax.set_title("Monty Hall Monte Carlo — Win Ratio Convergence")

ax.legend()

ax.set_ylim(0, 1)

plt.tight_layout()

plt.show()

Want to run this locally? With uv installed:

uv run --with numpy --with matplotlib monty_hall.pyOr copy the code blocks above into a Jupyter notebook and experiment — try changing the number of doors, the bet amounts, or the number of rounds.